The Federal Emergency Management Agency (FEMA) is updating the National Flood Insurance Program's (NFIP's) methodology for calculating NFIP flood insurance premiums. Risk Rating 2.0 is a new approach that will utilize the latest technology, updated data, and modern catastrophe modeling to provide rates that are actuarily sound, equitable, and reflects the flood hazard for each property's unique characteristics. Prior to Risk Rating 2.0, NFIP flood insurance policies have been based on national averages, which do not always reflect an individual property's actual flood risk and cost to rebuild. With Risk Rating 2.0, these inconsistencies are addressed by taking into account additional flood risk variables, which include flood frequency, river overflow, storm surcharge, coastal erosion, heavy rainfall, distance to a water source, property and structure attributes, and cost to reconstruct.

Since the 1970s, the NFIP's flood premiums have been based on relatively static measurements, emphasizing a property's elevation within a FEMA-mapped flood hazard area. Due to this antiquated method, current policyholders with lower-valued homes have been paying more than their shared risk while policyholders with higher-valued homes have been paying less than their shared risk. Risk Rating 2.0 considers the rebuilding costs, which allows FEMA to equally distribute rates amongst all policyholders based on the value of their home and the flood risks associated with the unique characteristics of their property.

Current NFIP policyholders and those seeking a new policy can contact their insurance company or insurance agent to learn more about what Risk Rating 2.0 means to their flood insurance rates.

Risk Rating 2.0 is being implemented in two phases:

Phase I

New policies - Beginning October 1, 2021, new policies will be subject to the new Risk Rating 2.0 rating methodology.

Existing policies - Existing policyholders renewing prior to April 1, 2022, will have two renewal options: base the insurance premium under the old methodology; or base the premium under the new Risk Rating 2.0 methodology, which may yield a lower premium.

Phase II

All remaining policies renewing on or after April 1, 2022, will be subject to the new Risk Rating 2.0 methodology.

What IS changing under Risk Rating 2.0

What IS NOT changing under Risk Rating 2.0

What IS Discontinued under Risk Rating 2.0

Frequently Asked Questions - Risk Rating 2.0

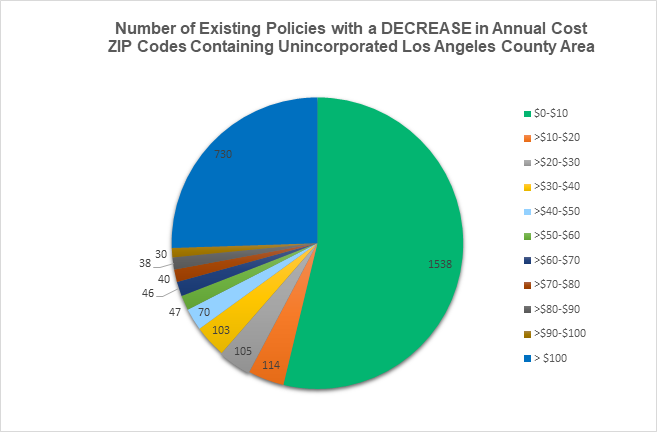

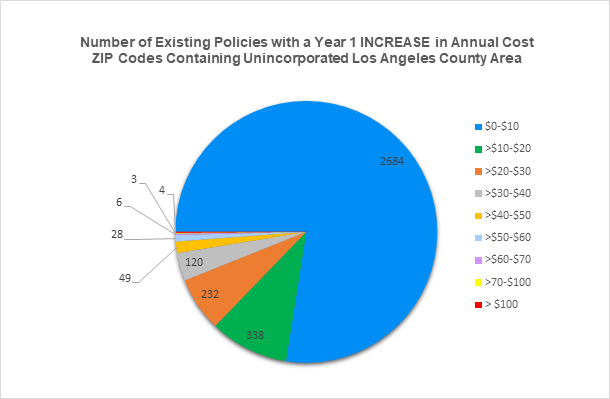

Cost Impact on Los Angeles County Unincorporated Areas

Existing policies facing full-risk (actuarial) rates that are higher than their current rate are on a transitional glidepath of annual increases of no more than 18% until the full-risk rate is reached. Depending on the amount of the full-risk rate, it can take several years to reach this rate. Below are summaries of information compiled from FEMA’s dataset on Risk Rating 2.0’s Year 1 impact on existing flood insurance policies in the ZIP codes that contain Los Angeles County unincorporated areas:

If you need further information, you can contact us at: FloodAnalysis@pw.lacounty.gov.

FEMA Links for Additional Information

Do you have a Preferred Risk Policy?

Discount Explanation Guide

Rate Explanation Guide

Renewing Flood Insurance Policies Under Risk Rating 2.0: Equity in Action

National Flood Insurance Program Flood Insurance Manual

National Flood Insurance Program Flood Insurance Appendices

National Flood Insurance Program: Risk Rating 2.0 Methodology and Data Resources

Risk Rating 2.0 State Profiles

Find an Insurance Form